พุทธบูรณาการเพื่อส่งเสริมการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี ภายใต้สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์

คำสำคัญ:

พุทธบูรณาการ, การปฏิบัติงาน, ผู้ประกอบวิชาชีพบัญชีบทคัดย่อ

บทความวิจัยนี้มีวัตถุประสงค์คือ 1. เพื่อศึกษาการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี 2. เพื่อศึกษาปัจจัยที่ส่งผลต่อการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี และ 3. เพื่อนำเสนอพุทธบูรณาการเพื่อส่งเสริมการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชีภายใต้สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์ ดำเนินการตามระเบียบวิธีวิจัยแบบผสานวิธี คือ การวิจัยเชิงปริมาณเก็บข้อมูลด้วยการแจกแบบสอบถามกับกลุ่มตัวอย่างจำนวน 395 คน การวิจัยเชิงคุณภาพโดยวิธีการสัมภาษณ์เชิงลึกกับผู้ให้ข้อมูลสำคัญ จำนวน 18 รูปหรือคน การวิเคราะห์ข้อมูล เป็นการวิเคราะห์ข้อมูลเชิงพรรณนา และการวิเคราะห์การถดถอยพหุคูณแบบขั้นตอน (Multiple Regression Analysis) ด้วยโปรแกรมสำเร็จรูปทางสถิติ และสัมภาษณ์เชิงลึก วิเคราะห์ข้อมูลโดยการวิเคราะห์เนื้อหาเชิงพรรณนาเพื่อยืนยันผลการศึกษาเชิงปริมาณจากผู้ให้ข้อมูลสำคัญอีกครั้งหนึ่ง

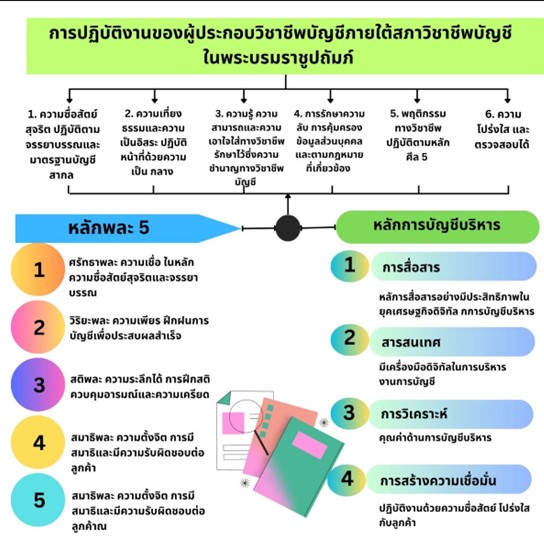

ผลการวิจัยพบว่า 1. การปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี โดยภาพรวมอยู่ในระดับมาก (=4.20) เรียงตามลำดับดังนี้ ด้านพฤติกรรมทางวิชาชีพ ด้านการรักษาความลับ ด้านความซื่อสัตย์สุจริต ด้านความรู้ ความสามารถและความเอาใจใส่ทางวิชาชีพ ด้านความเที่ยงธรรมและความเป็นอิสระ และด้านความโปร่งใส ตามลำดับ 2. ปัจจัยที่ส่งผลต่อการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี พบว่า หลักการบัญชีบริหารส่งผลต่อการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี ประกอบด้วย การวิเคราะห์ การสื่อสาร การสร้างความเชื่อมั่น อย่างมีนัยสำคัญทางสถิติที่ระดับ 0.01 ส่วนสารสนเทศ มีนัยสำคัญทางสถิติที่ระดับ 0.05 และหลักพละ 5 ส่งผลต่อการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชี ประกอบด้วย ปัญญา ความรู้ทั่ว วิริยะ ความเพียร สมาธิ ความตั้งจิตมั่น สัทธา ความเชื่อ อย่างมีนัยสำคัญทางสถิติที่ระดับ 0.01 ส่วนสติ ความระลึกได้ มีนัยสำคัญทางสถิติที่ระดับ 0.05 3. พุทธบูรณาการเพื่อส่งเสริมการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชีภายใต้สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์ คือการนำหลักพละ 5 เข้ามาบูรณาการ ประกอบด้วย ศรัทธาพละ ความเชื่อ วิริยะพละ ความเพียร สติพละ ความระลึกได้ สมาธิพละ ความตั้งจิต และปัญญาพละ ความรู้ทั่ว นอกจากนั้นยังนำหลักการบัญชีบริหารมาเป็นพื้นฐานในการส่งเสริมการปฏิบัติงานของผู้ประกอบวิชาชีพบัญชีทั้ง การสื่อสาร สารสนเทศ การวิเคราะห์ และการสร้างความเชื่อมั่น

เอกสารอ้างอิง

เจตน์ ตันติวณิชชานนท์. (2557). บทบาทของพระพุทธศาสนาในการพัฒนาชาติ : มุมมองของอาจารย์ป๋วย อึ๊งภากรณ์. วารสารสันติศึกษาปริทรรศน์, 4(2), 341-355.

พิมพาภรณ์ พึ่งบุญพานิชย์. (2560). แนวทางการจัดทางานวิจัยด้านการบัญชีบริหาร. วารสาร มจร สังคมศาสตร์ปริทรรศน์, 6(4), 72-86.

มหาวิทยาลัยมหาจุฬาลงกรณราชวิทยาลัย. (2539). พระไตรปิฎกฉบับภาษาไทย ฉบับมหาจุฬาลงกรณราชวิทยาลัย. กรุงเทพฯ: โรงพิมพ์มหาจุฬาลงกรณราชวิทยาลัย.

ยลวรรณ จิรวัชรเดช. (2567). 3 วิธีปรับตัวที่นักบัญชียุคใหม่ต้องมี ให้พร้อมรับมือกับความเปลี่ยนแปลง (Flow Account, 2563). สืบค้น 2 มกราคม 2567, จาก https://flowaccount.com/blog/3-ways-to-adapt-as-an-accountant/

วรินทร จินดาวงศ์. (2566). การบูรณาการหลักพุทธธรรมเพื่อส่งเสริมประสิทธิภาพการปฏิบัติงานของบุคลากรในสังกัดสำนักงานศึกษาธิการจังหวัดศรีสะเกษ (ดุษฎีนิพนธ์ปรัชญาดุษฎีบัณฑิต สาขาวิชารัฐประศาสนศาสตร์). พระนครศรีอยุธยา: มหาวิทยาลัยมหาจุฬาลงกรณราชวิทยาลัย.

สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์. (2566). TFAC Annual Report 2023 รายงานประจำปี 2566, สถิติการจัดอบรม/สัมมนา ประจำปี 2566 (1 มกราคม - 31 ธันวาคม 2566: แยกตามด้านวิชาชีพบัญชีและสำนักงานสาขา). กรุงเทพฯ: สภาวิชาชีพบัญชี ในพระบรมราชูปถัมภ์.

สิงห์คำ มณีจันสุข. (2562). การบริหารจัดการสวัสดิการสำหรับคนพิการทางการเคลื่อนไหวหรือทางร่างกายขององค์กรปกครองส่วนท้องถิ่น (ดุษฎีนิพนธ์ปรัชญาดุษฎีบัณฑิต สาขาวิชารัฐประศาสนศาสตร์). พระนครศรีอยุธยา: มหาวิทยาลัยมหาจุฬาลงกรณราชวิทยาลัย.

AMTgroup. (2567). จรรยาบรรณของผู้ประกอบวิชาชีพบัญชี สำคัญอย่างไร?. สืบค้น 11 กันยายน 2567, จาก https://www.amtaudit.com/view_news.php?id=30.

Yamane, T. (1973). Statistic: An Introductory Analysis. (3rd. ed.). New York: Harper and Row.