The Marketing Mix affect the Confidence in Selecting the People's Bank Project Loan Service to Solve Informal Debt of The Government Saving Bank, Tha Wung Branch

Article Sidebar

Main Article Content

Abstract

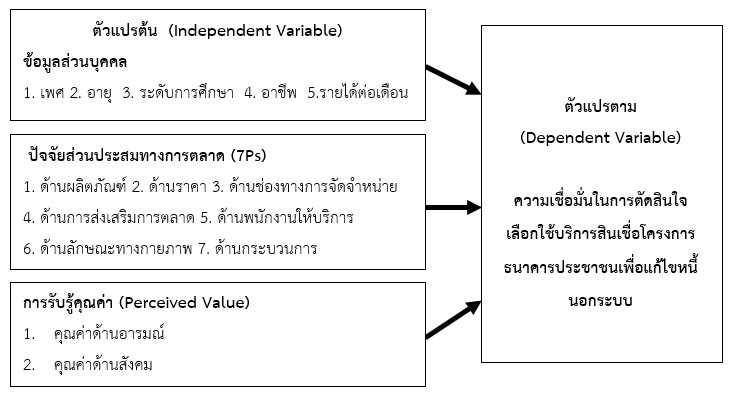

The objectives of this study were to study how gender, age, occupation, monthly income, marketing mix, and perceived value affect confidence in selecting the People's Bank project loan service to resolve informal debt. Sample, group: 333 people, using a questionnaire to collect data from a sample of 333 people, using Taro Yamane’s calculation formula, and data were analyzed using frequency, percentage, mean and standard deviation. One-way ANOVA, independent t-test and multiple regression at a statistical significance level of 0.05. The results of the study found that most respondents were female, aged 30-39 years, and were employed by a private company with an average monthly income of 15,001-30,000 baht. Most of them are still owed no more than 50,000 baht in debt payments outside the system. Because there is not enough money to cover daily expenses, the debt is overdue in the system. The purpose of choosing the People's Bank project loan is to solve informal debt because you want to close informal debt. Confidence in selecting the People's Bank project loan service to resolve informal debt is at the highest level. Age has a statistically significant effect on confidence in choosing the People's Bank project loan service to resolve informal debt. The marketing mix factors have a statistically significant effect on confidence in choosing the People's Bank project loan service to resolve informal debt of the Government Saving Bank, Thawung Branch, which were significantly different, including loan service staff factors and process factors. Factors of perceived value have a statistically significant effect at the 0.05 level on confidence in choosing the People's Bank project loan service to resolve informal debt of the Government Saving Bank, Thawung Branch, including social value and emotional value. Guidelines for increasing credit balance are creating a bond and satisfaction that will make customers feel even more confident in using the Government Saving Bank’s loan services, Thawung Branch.

Article Details

References

เกษรา กองแก้ว. (2563). ศึกษาปัจจัยส่วนประสมทางการตลาด (7Ps) ที่มีอิทธิพลต่อการเลือกใช้บริการสินเชื่อเงินด่วน A-cash ของธนาคารเพื่อการเกษตรและสหกรณ์การเกษตร สาขาเลิงนกทา [การค้นคว้าอิสระปริญญามหาบัณฑิต]. มหาวิทยาลัยรามคำแหง.

ธานินทร์ ศิลป์จารุ. (2552). การวิจัยและวิเคราะห์ข้อมูลทางสถิติด้วย SPSS และ AMOS (พิมพ์ครั้งที่ 13). วี. อินเตอร์ พริ้นท์.

นธกฤติ วันต๊ะเมล์. (2555). การสื่อสารการตลาด Marketing. มหาวิทยาลัยเกษตรศาสตร์.

มณทิรา น้อยจีน. (2562). ปัจจัยส่วนประสมทางการตลาดที่ส่งผลต่อการตัดสินใจใช้บริการ Krungthai NEXT ของลูกค้าธนาคารกรุงไทย จำกัด (มหาชน) จังหวัดนครปฐม [การศึกษาอิสระปริญญามหาบัณฑิต]. มหาวิทยาลัยรามคำแหง.

รอชิด้า ยีสมาน. (2564). ปัจจัยที่มีผลต่อการตัดสินใจเลือกใช้บริการทางการเงินผ่านทาง Mobile Banking Application ในสถานการณ์ COVID-19 [การค้นคว้าอิสระปริญญามหาบัณฑิต]. มหาวิทยาลัยรามคำแหง.

ศรัญญา หล้ามุงคุณ. (2564). ปัจจัยที่ส่งผลต่อการจัดสินใจใช้บริการสินเชื่อที่อยู่อาศัยธนาคารอาคารสงเคราะห์ สำนักงานใหญ่ ของลูกค้าที่พักอาศัยอยู่ในกรุงเทพมหานคร [การค้นคว้าอิสระปริญญามหาบัณฑิต]. มหาวิทยาลัยรามคำแหง.

สิริรัก บุญมี. (2562). ปัจจัยส่วนผสมการตลาดกับกระบวนการตัดสินใจเลือกใช้บริการสินเชื่อประเภทโครงการธนาคารประชาชนของธนาคารออมสิน จังหวัดชุมพร. วารสารสหวิทยาการวิจัย ฉบับบัณฑิตศึกษา, 8(1), 1-2.

สำนักข่าวอินโฟเควสท์. (2567, 15 มีนาคม). ออมสิน-ธ.ก.ส. อนุมัติสินเชื่อช่วยลูกหนี้นอกระบบแล้ว 525 ราย ยอดหนี้ 12 ลบ. https://www.infoquest.co.th

อลิสา หมีดเส็น. (2562). การรับรู้คุณค่าการบริการของลูกหนี้ร่วมที่มีผลต่อความตั้งใจใช้บริการสินเชื่อในอนาคต กรณีศึกษา ธ.ก.ส. สาขาหาดใหญ่ [วิทยานิพนธ์ปริญญามหาบัณฑิต]. มหาวิทยาลัยสงขลานครินทร์.

Pavlou, P.A., Liang, H., & Xue, Y. (2007). Understanding and mitigating uncertainty in online exchange relationships: A principal-agent perspective. Management Information Systems Quarterly, 31(1), 105–136.

Sweeny, J.C., & Soutar, G. (2001). Consumer perceived value: The development of multiple item scale. Journal of Retailing, 77(2), 203-22.